|

|

FIRM CAPITAL PRIVATE CLIENT REPORT

|

|

|

|

|

|

|

DEVELOPMENT & CONSTRUCTION - OCTOBER 2019

|

|

|

|

Co-Written By Ben Myers of Bullpen Research & Consulting Inc.

|

|

|

|

|

TORONTO & VANCOUVER HOUSING MARKETS

|

|

|

|

|

|

|

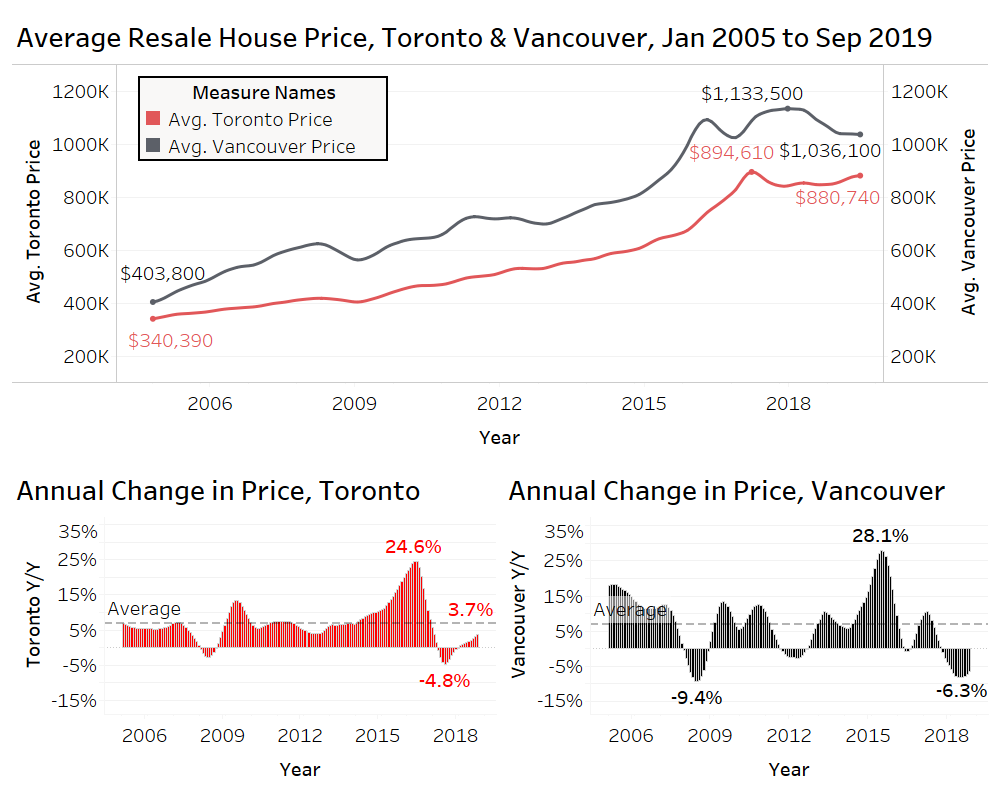

Resale House Prices

The chart above shows the average resale house price in the Greater Toronto and Greater Vancouver areas from January 2005 to September 2019 via data from the Brookfield RPS House Price Index. In June of 2017, Toronto hit a high-water mark of nearly $895,000, with annual growth hitting 25% a month earlier. The average priced dropped $50,000 by February 2018 and stayed flat for year. The market has slowly improved, increasing by 3.7% year-over-year in September 2019. Prices have now increased for 10 consecutive months. Economist Will Dunning noted that new listings in the market are too low, and the sales-to-new listings ratio suggests future price growth.

The Vancouver market has been much more volatile than Toronto, with the average resale price increasing by 28% in May of 2016, before going negative a year later. Prices bounced back sharply

in 2018, hitting a market-high of $1.13 million in March of that year, before losing $100,000 in value by September 2019. Vancouver resale transactions jumped 46% annually in September 2019, however, September 2018 sales had fallen 43% annually. Confidence is returning to the market, but Royal Lepage recently stated that "Buyers are in control in the detached market" and that "Higher inventory levels in some areas are offering buyers multiple options to choose from,” before concluding that “these days may be coming to an end."

|

|

|

|

|

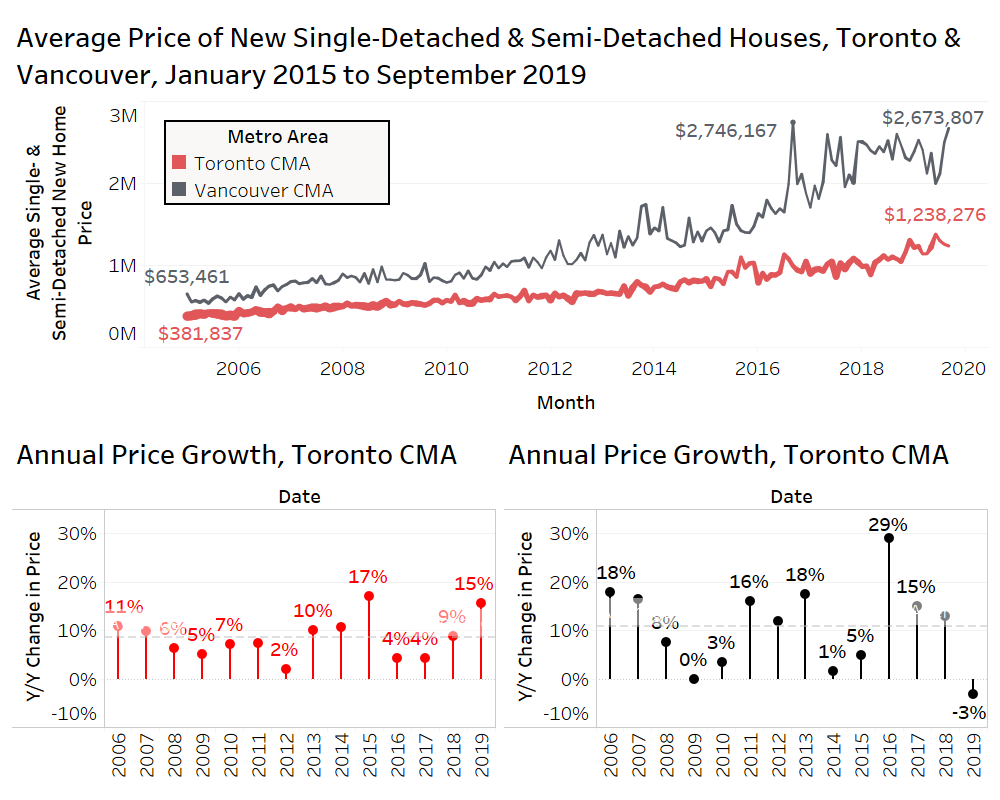

New Home Prices

In September 2019, the average new single-detached and semi-detached home in the Toronto CMA averaged $1.24 million (price recorded at closing), an increase of 15% from a year earlier. Given the recent sales slump, the 15% annual price growth reflects many homes with longer closings, that sold when the market was stronger. However, there have been some recent successful low-rise new home launches, but absorption remains well below the frenzied 2015/2016 levels. For the first time in 10 years, the average price of a new single-family home in the Vancouver CMA has declined annually. The 3% annual decline is a significant departure from the long-run average of 11% annual growth experienced since 2005, and the 29%

year-over-year jump in 2016. Despite hitting a 5-year high of 1,287 completed and unsold new single-family homes earlier this year, standing inventory dropped to 1,092 in September, showing there is still demand for the $2 million-plus new single-detached market in the metro area.

|

|

|

|

|

|

|

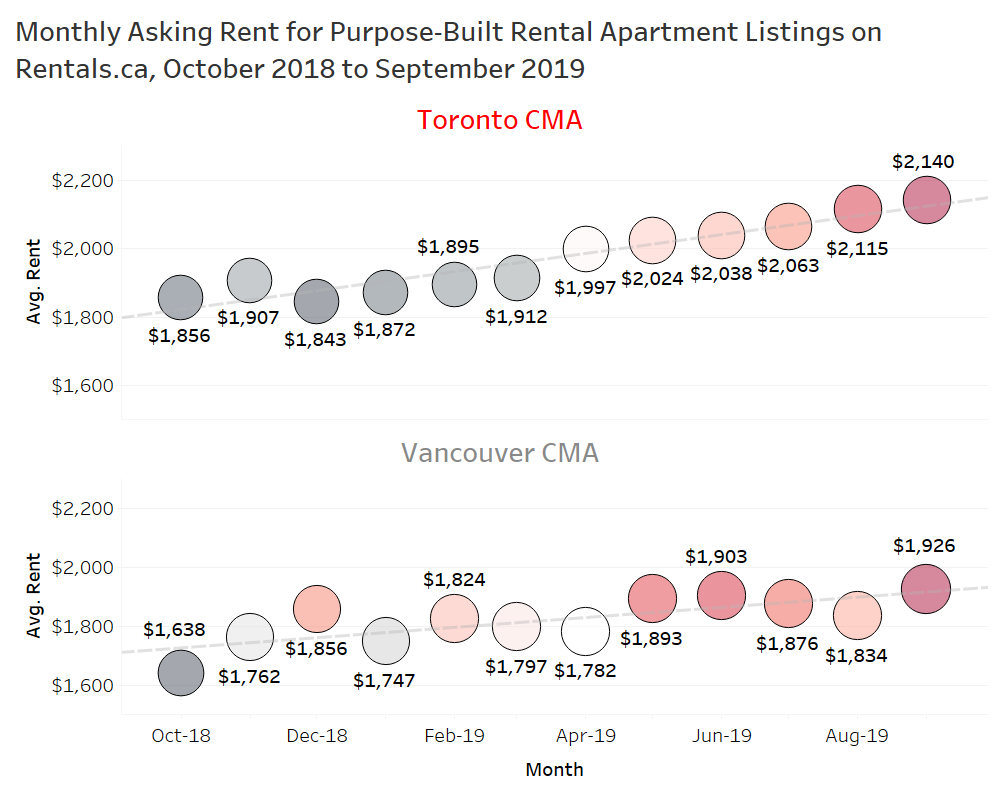

The Rental Market

RBC Economics recently published on a report on the state of the rental market in Canada, noting that the Toronto CMA needs 9,100 more vacant units to reach a "healthy" vacancy level of 3%. Vancouver needs 3,800 more available units. The vacancy rate has been at historically low levels for rental apartments and condo apartments in these two metro areas for several years. The recent rise in interest rates, the new stress test, and rising prices for entry-level product have resulted in rapid growth in rental rates. The chart above shows the average asking rent for vacant rental apartment units in the Toronto and Vancouver CMAs based on data from online rental listings portal Rentals.ca. From October 2018 to September 2019,

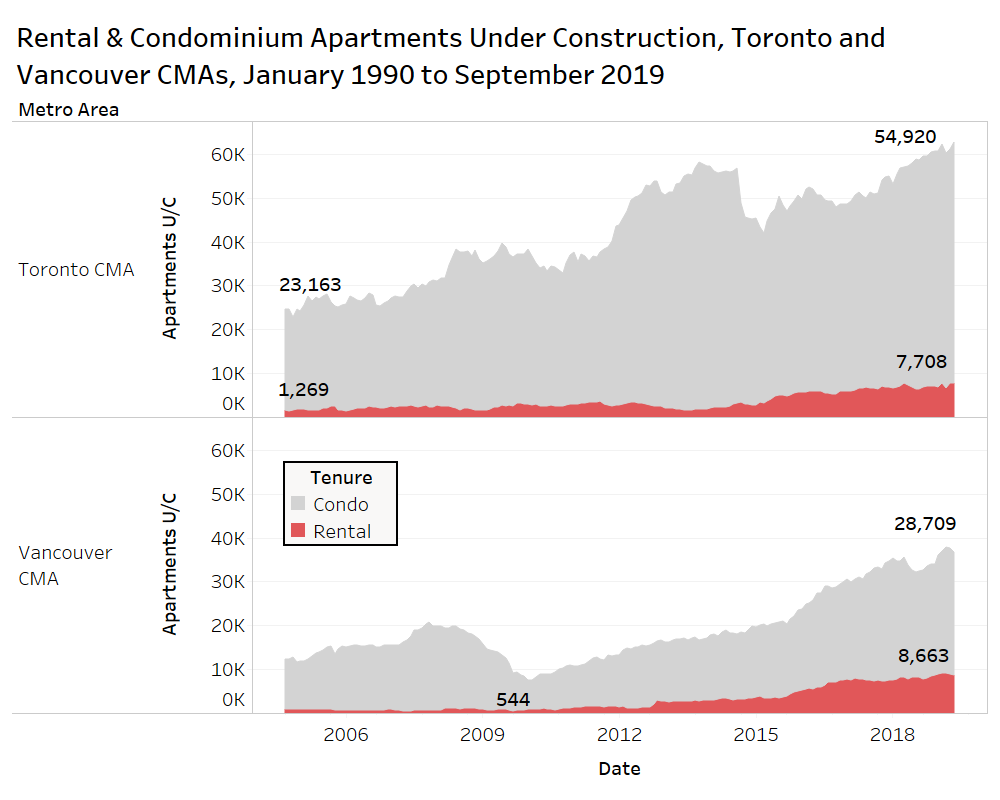

the average rental rate has risen approximately 15% in the Toronto CMA from about $1,860 to $2,140 per month. In Vancouver, rent inflation is lower, but still very strong, increasing by 10% annually from about $1,640 to $1,930. Developers and their financial partners are taking notice, and there are more rental apartments under construction in the Toronto and Vancouver CMAs in September 2019 than any other time over the past 30 years (see the chart below). In addition to the rental apartments being built, these markets have a near-record high level of condominium apartments under construction. Given this reality, there may be concerns regarding oversupply, however in Toronto that is a long way off from

occuring. According to the RBC study, the Toronto CMA needs 22,000 new rental apartments and rented condo apartments per year to satisfy demand between 2019 and 2023. Vancouver needs 9,400 annual rental units per RBC. Over the next couple years, the Toronto CMA will deliver about 17,000 to 22,000 new condos and 2,500 to 3,000 new purpose-built rental apartment (PBR) units per year. If we assume an aggressive investor share of condos at 70%, the market would add about 15,000 leased condos and 3,000 PBR units for 18,000 total rented apartments annually, still 4,000 units under the demand level projected by RBC.

In the Vancouver CMA, 11,000 to 13,000 condos are coming and around 5,000 rental units per year based on recent starts data. So the metro are could add as many as 12,000 to 14,000 new rented apartment units per year, far

exceeding the 9,400 units of demand, and potentially eating up all of the 3,800 units of undersupply required to raise the vacancy rate to 3%. Vancouver could experience flat or declining rent levels depending on the level of "induced demand" - as supply increases, rents decline, and people could decide to move to Vancouver that wouldn't have in the absence of these conditions.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

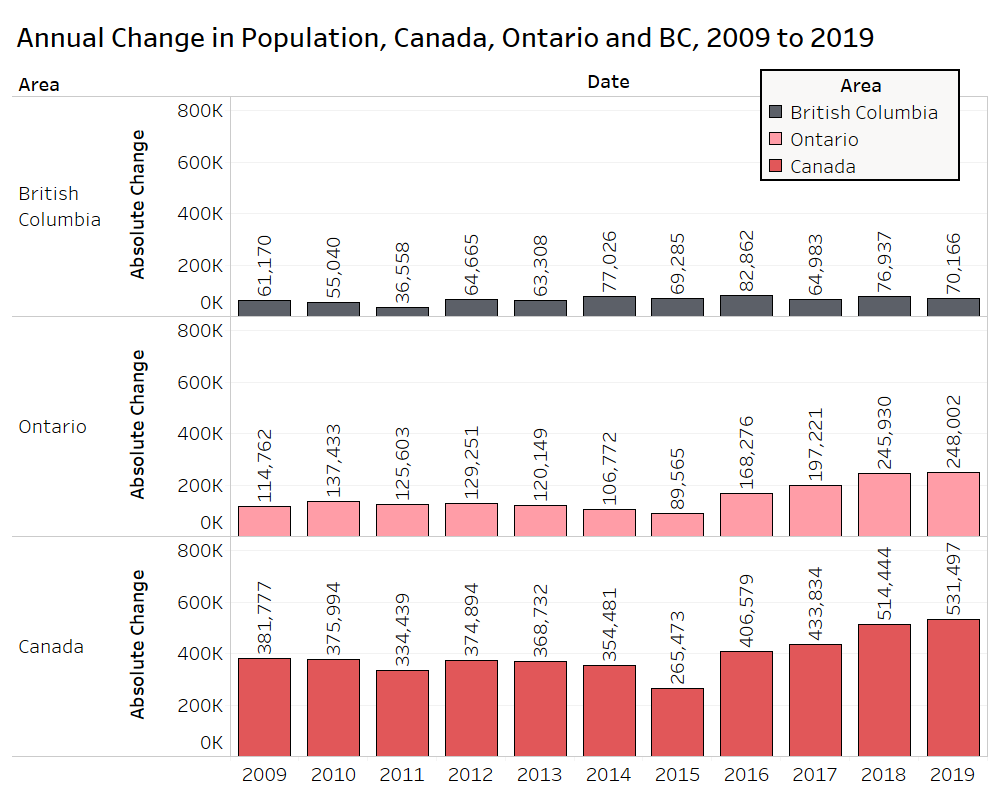

The historical averages used to project housing demand in Toronto and Vancouver may be underestimated, as population growth continues to set records. According to Statistics Canada, the annual increase in population nationally of approximately 531,000 people from August 2018 to July 2019 was the largest one-year increase ever recorded (see chart above). The 10-year average is approximately 400,000.

In British Columbia, the growth of 70,000 people annually is only slightly above the long-run average of 65,000. In Ontario, population grew by almost 250,000 people, nearly 100,000 more than the 10-year average of 155,000. Nearly 60% of the national population growth in Canada occurred in BC and Ontario.

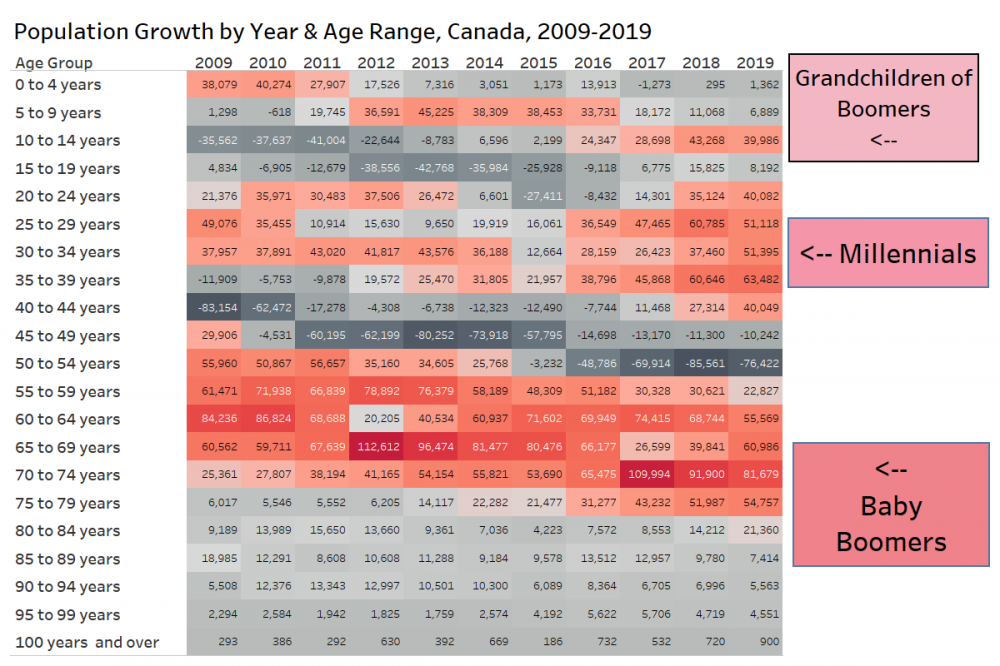

The shifting demographics in Canada will continue to impact the housing market, as boomers retire, move-down to smaller properties, or cash-out and move away from large municipalities. The millennials, often referred to as the echo-boomers,

are moving up from the rental market to the ownership market, or buying their second home. These are the two major population waves impacting the market. However, a third wave is coming, as the grandchildren of boomers are about 3-5 years away from going to university or college and taking their first step up the property ladder. This "Generation Z" will be looking for student housing, basement apartments, studio apartments, and chopped-up single-family properties, impacting the already precarious housing situations of the least affluent in our communities.

The "red streaks" in the chart below, which plots the increase in population by year and age groupings in Canada from 2009 to 2019, shows how the boomers, their children, and their grandchildren are impacting growth.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

ATTENTION BUILDERS:

Firm Capital will provide financing for your purchasers that do not qualify for a mortgage because of the new bank rules. Please click on the link below for details of our program.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

For 30 years Firm Capital has specialized in providing mortgage lending and equity capital to builders and developers for land, land servicing, infill construction, hi-rise/mid-rise/multi-family construction projects, and builder inventory loans.

|

|

|

|

|

|

|

|

|

|

Distributed exclusively to private clients of Firm Capital.

|

|

|

|

|

|

|

You are receiving this email because you are a private client of Firm Capital Corporation. Unsubscribe

|

|

|

|

|

|

|

Firm Capital Corporation

163 Cartwright Avenue,

Toronto, ON M6A 1V5

Canada

(416) 635-0221

www.FirmCapital.com

|

|

|

|

|

|

|